Long Term Wealth Creation - How to 100x my Money in 20 Years

Long Term Wealth Creation - How to 100x my Money in 20 Years

100x'ing my Money in 20 years

TL;DR: In order to 100x my Net Worth (NW) in 20 years I need to grow it by 26% per year. After evaluating various options, I’ve concluded that my best bet is to build/buy a portfolio of entrepreneurial ventures with varying probabilities of success and size of pay-out.

Read more to know about my thought process.

Topics Covered

My Financial Goals: 10x vs. 100x vs. 1000x Returns

The End of Wealth Accumulation

Era of Wealth Creation

My Strategy on a Portfolio of Small Bets

What are my Entrepreneurial Bets Right Now?

LET’S START

Recently, my wife and I decided to buy our first apartment and the only thought in my mind has been, “How the hell are we going to pay these EMIs?”

I started my personal finance journey early in my career. Thanks to the stock market rally in 2020 (and some timely purchases in March 2020), I was able to meet a significant milestone in my wealth accumulation journey this past year. This happened because of consistent investments in the last 8-9 years.

However, as a 31 Year old with a plan to a buy an apartment, I realised I needed to look at my finances from a long-term perspective. The first step to that was defining my goals and understanding if my current plan of action is enough to keep me on track to achieve those goals.

I needed to seriously think through my long term plans for building wealth.

As I wrote down my goals, I quickly realised that to reach these goals, I will have to completely change the way I look at money so that I can 100x my Net Worth (NW) in 20-30 years instead of just 10x’ing it through investments and accumulation. I realised that I need to Create Wealth instead of just Accumulating it.

My Financial Goals

I have a solid number in mind, but I’ve kept it vague here.

My overall goal is to ensure that my family can afford a comfortable lifestyle without any active streams of income within 20 years. Adjusting for inflation, that number needs to be at least 100x of my Current Net Worth.

Note: Inheritance is excluded from this entire discussion.

10x vs. 100x vs. 1000x Returns

I started playing with different compound rate calculators to get a sense of what interest rates I would need in order to hit these goals.

A 12.5% annual increase in my NW will give me ~10x returns over 20 years 🙂

26% will give me ~100x returns over 20 years 😁

41% will give me ~1000x returns over 20 years 🤩

So how do I plan for a 26% year on year increase in my net worth over a 20 year horizon?

To explore this, I had to think back about what I’ve already done with my money

My Financial Journey so Far

I’ve been saving money for the past decade.

I’ve saved it in my bank account, invested it in mutual funds, bought individual stocks, and have explored almost every single investment option within India (and some abroad). One of my proudest achievements was foreseeing the rise in a particular infrastructure stock and getting a 50% return in a week.

However, the biggest driver increasing my savings year over year were not the returns from my investments but rather the increase in my salary. Since my salary was a significant percentage of my NW, I’ve been able to save every year and grow my savings quickly – exceeding the 26% YoY that I didn’t even know I needed.

My investments gave me only 12% returns but it didn’t matter because my overall NW was increasing at a much faster rate.

What have I learnt?

Essentially, this was my era of Wealth Accumulation. I accumulated my salary, put that money into safe/medium risk investments and I let them passively, slowly accrue. Unknowingly, I was building the capital which will now be the foundation of my Wealth Creation journey.

The cycle of wealth accumulation will end in a year or two because:

a) My expenses are slated to increase in a few years if I start a family (just getting a dog significantly increased my expenses – but totally worth it).

b) My salary as a % of NW will become smaller.

I needed to change the way I was thinking about my long run wealth.

Era of Wealth Creation

While the accumulation strategy has helped me build a safety net in the first phase of my career, I realise that in order to meet my financial aspirations, I need to move in the era of Wealth Creation by taking risks. Below is a summary of the options that I considered for creating wealth.

The Barbell Investment Strategy

I recently learnt of the ‘Barbell Investment Strategy’ while listening to this podcast with Chamath Palihapitiya. This strategy states that ‘the best way to strike a balance between reward and risk is to invest in the two extremes of high risk and no risk assets while avoiding middle-of-the-road choices.’

If I apply this framework to myself – I have put most of money in the safe and middle-of-the-road assets but have very little in high risk assets. This is why I am attracted to this framework - it gave me a new way to think about my investment and risk taking strategies that aligned with my entrepreneurial bent.

Using this framework, if I want my Net Worth to increase by 26% YoY, and I’ve received only 10-12% returns from current investments, my high risk assets would need to provide me with outsized returns that far exceed 26%.

There are very few (if any) asset classes that provide >30% returns, year on year.

Understanding this strategy has reinforced the need to move into an era of Wealth Creation if I have to meet my goals.

What are my investment options?

This article clearly lays out all the options for growing one’s wealth. I would really recommend that everyone read it.

My major options:

a) Salary

b) Equity

c) Debt (not going to consider this except as leverage to build equity)

Salary

My current salary will allow me to build my wealth by 10-20% for the next few years but beyond that, I will need a significant salary hike each year in order to match my requirements. Unless I make a career change and become an investment banker - I don't see this happening.

Equity

i) Bond Market

ii) Stock Market

iii) Private Equity

iv) Venture Capital

v) Entrepreneurship (or working with a startup)

The Bond & Stock Market can be used on the risk-free (relatively) side of the barbell if I invest for the long-term (10+ Years). Day trading (high risk/high return) is not my forte.

Private Equity can give me good returns in the long run but I don't have enough capital.

Venture Capital is where my thoughts were at the start of 2020. Everyone is making money with start-ups – I’m smart, why can’t I do it? I even wrote down a personal goal at the start of the year to invest in at least one start up.

This fantastic Twitter thread was the start of the end of that startup investor dream in me. Over the past 4 months, I’ve repeatedly thought about the points made in this thread and my belief in its accuracy (for a small investor like me) has strengthened. Angel Investments are part of the risky side of my barbell - I may invest in industries where I have a unique insight or if I know the founders really well. But this is not my focus area. Syndicate investing may also make sense.

Entrepreneurship, in my opinion, is the riskiest asset class but also the one with the capabilities of providing outsized returns of 30%+ Return on Equity over the long run.

It took me a long time to get to this conclusion – but I realised that if I wanted to hit my net worth goals, 100x my capital, and move into an era of Wealth Creation, I needed to build the risky side of my barbell by using my capital to build businesses.

Do I want to build the next Unicorn 🦄?

In order to build an Unicorn, there’s no doubt that I’ll have to go raise VC money. The way I see it - each extra dollar raised has an additional probability of failure attached to it as you have to give a bigger exit to the investors.

A venture capital funded business with a 0.1% chance of reaching a billion dollar valuation is a risky endeavor where I don’t want to bet 5-10 years of my time and my life savings. I would rather play in the realm of real possibilities. The way I see it, a lot of VC funded businesses could’ve been profitable, cash flow generating businesses if not for the capital they raised. And I aim to build those kind of businesses.

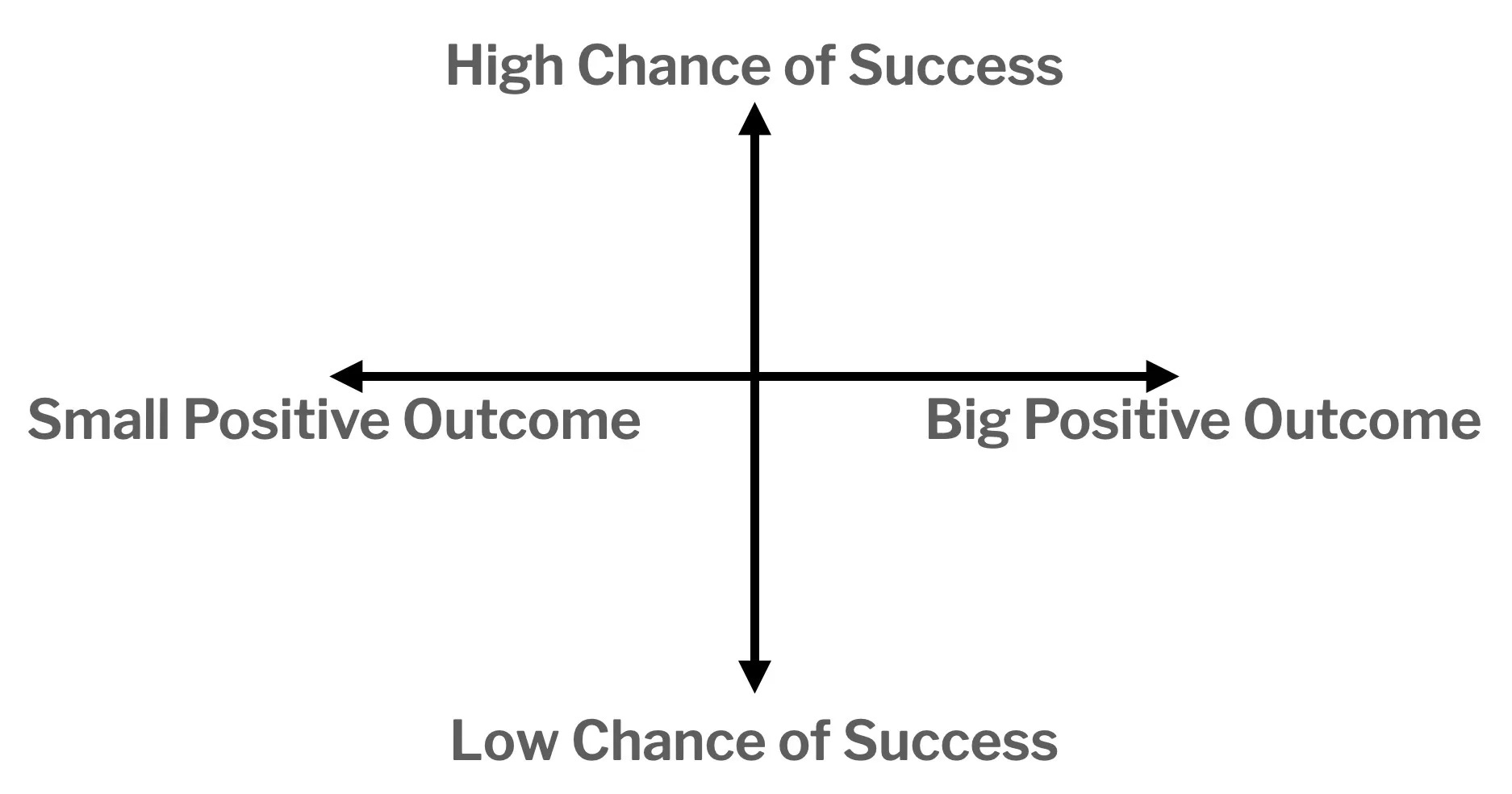

Seth Godin’s Matrix of Choices

While I was writing all this, Seth Godin published this article that articulates this thought on probabilities and outcomes much better than I can. It’s a pretty short read, I highly recommend reading it. Seth talks about various traps that you should avoid by over-investing your time/money into a single quadrant of the grid below.

“Consider a portfolio of projects. Some of them have a very high likelihood of working out, and each one of these outcomes is pleasant, if not game-changing. Play often enough, though, and your persistent generosity will pay off.”

He calls the grid below a ‘A simple 2 x 2 for choices’.

The biggest pushback I’ve heard on my Portfolio of Small Bets strategy is the importance of focus. I intend to get a better handle of this as things evolve, but the idea is to rely on Personal Leverage to work with some young leaders who can run some of these small businesses (once they’re larger).

A Collection of Small Businesses - Other People Have Done It

My favourite business model of the decade: Tiny Capital.

“Tiny Capital starts, buys, and invests in Internet-based businesses. Tiny has either founded or acquired over 25 tech companies.”

Another similar company: Thrasio

“We buy and grow Amazon businesses”

How Can I build a Portfolio of Entrepreneurial Bets?

“Give me a lever long enough and a fulcrum on which to place it, and I shall move the world.” - Archimedes

In order to build a significant business, I can use the following leverages. I’d written a lot more about leverages but I took it out - I will write a separate article just about leverages and how I plan to use them.

1) Labour Leverage - 👔👔👔

2) Capital Leverage - 💰💰💰

3) Product & Media Leverage - 🎙️🎙️🎙️

“(P)roducts (and media) that have no marginal cost of replication.”

4) Personal Leverage - 🛠⚒🛠⚒

The ability to 10x your productivity by using automation or delegation.

Labor and Capital Are Old Leverage by Naval– really good article, read it.

Product and Media are New Leverage by Naval – continuation on the previous article.

Personal Leverage: How to Truly 10x Your Productivity by Nat Eliason.

What are my Entrepreneurial Bets Right Now?

Equity in my company.

My biggest bet with the largest possible payout.

Classic capital & labour leverage.

Podcast & Newsletter.

Trying to be an influencer (I guess?) has a big positive outcome if done right but there are so many other people playing this same game.

Media Leverage.

Not sure on where this falls in Seth’s Matrix as we’re still trying to figure out the long-term play here.

Home Decor E-Comm Business.

I made this website 2 years ago and promptly ignored it - I get a few thousand dollars of revenue per year, barely covering Shopify’s costs. I’ve picked it back up in the past few weeks and am trying to fix it.

The dropshipping/ecomm model is easy to enter and thus overly competitive.

Small positive outcome with a low chance of success - I may be wasting my time on this since I’m not clear on the leverages.

Is the leverage media for SEO? Capital? I’m not sure.

I’m just using this to get better at SEO/E-Comm in general.

Group purchase of an US E-comm Business (still deciding).

Higher revenue & an industry which is likely to explode.

SEO of this website is well established and can thus be used to scale up.

High chance of success with a moderate payout in my opinion.

Group purchase of Micro-SaaS Businesses (early stages).

Product Leverage

Difficult to predict the probability of success unless we acquire and scale one. But, do think this can lead to big positive outcomes when it comes to meeting my financial goals.

So Should I Buy that New Apartment?

Looking at this asset purchase from the lens of everything I’ve already written, buying a new apartment would count as a Low Risk asset on my financial barbell. If I want my long term vision to play out, I should liquidate my low risk assets and invest them into the apartment while paying a portion of my income as an EMI for the apartment.

However, I would need to ensure that I’m either apportioning a similar amount of money every month towards a high risk asset (capital leverage towards high risk investing or entrepreneurship) or that I’m using the product/media leverage to increase my net worth.

I’m probably going to buy that new apartment - just saw a few that I loved.